[Part 2/2] An In-Depth Note on Palantir Technologies ($PLTR) ─ The Next Nvidia?

- J

- Oct 21, 2024

- 17 min read

Updated: Jan 15

Update: Changes to the Excel models, due to a slight calculation error. Updated on October 22nd.

An analysis of $PLTR and the future potential. This is Part 2 of the in-depth note on Palantir. Before reading this, I highly recommend reading Part 1. This is not a stock recommendation and I strongly encourage everyone to do their own research.

Structure of the Entire $PLTR Note

Part 1/2

Introduction and General Background

Understanding the Business and the Unique Value Proposition

Understanding the Go-to-Market Strategy

Part 2/2

Zooming Out, Looking at Palantir in the Context of the AI Revolution

Stock Performance, Valuation, and Financials

Final Words

Zooming Out, Looking at Palantir in the Context of the AI Revolution

There is no doubt that we are in a time of change driven by rapid technological development. November 30th, 2022, with the introduction of Large Language Models (LLM's) to the general public, transformed the technology landscape.

The Earlier Computing Revolution and the Mobile Internet Value Chain

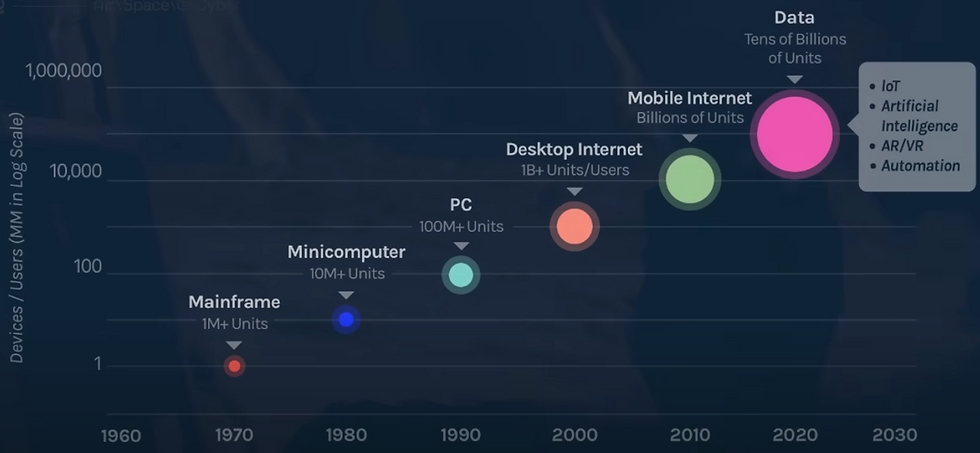

Is it possible to look back in time to gain a better understanding of what's to come? Maybe, maybe not. There are some interesting aspects to consider though. Looking at the computing revolution from the 1970s onwards, it went through several phases, going from 1M+ mainframe units to the billions of data units we see today. The exponential increase has been incredible.

Let's dive deeper into the last "completed" computing period, i.e the mobile internet value chain. In the beginning of this period, the critical core infrastructure for the mobile revolution had to be provided. Qualcomm was at the center of mobile connectivity with its Snapdragon processors and LTE modem technology, ensuring our devices could connect efficiently and reliably (The Verge, 2018). Meanwhile, ARM offered power-efficient chip architectures that became the standard for mobile devices, allowing companies like Apple and Samsung to build high-performance smartphones that wouldn’t drain their batteries. This pattern; starting with the critical infrastructure, then a technology stack including foundational software and data providers (Apple, Samsung, etc), and finally applications and services (Google, Meta, etc), is one that we’re likely to see as other technology revolutions take place, such as the current AI revolution. It will absolutely not be the same, but I think it's reasonable to expect some resemblance in terms of the phase ordering.

The Phases of the AI Value Chain

To gain a clearer and tangible understanding of where we are right now in the AI revolution, lets zoom out a little bit. The image immediately below paints a picture of the overall landscape for the AI value chain.

Broadly speaking, we can divide the value chain into three main phases, similar to what was described above for the mobile internet.

Foundational Infrastructure - Established

Core Technology Stack - Emerging

Applications & Services - Emerging

The difference with the AI value chain is that the exponential effects and the data dividend in this revolution is likely to be much greater. The branching and network effects of each technological development and associated capex' will be significant. This is very exciting from a value-creation perspective. So far in the early stages of the AI "gold rush", the clear winners have been the "pick-and-shovel" providers, i.e the companies supplying the critical tools and infrastructure necessary for AI development. Leading this pack are the semiconductor and chip providers, with Nvidia standing out as the hugely dominant force. Thanks to its GPUs, which power nearly all AI applications, Nvidia has cemented its position at the forefront of the AI hardware market. AMD and Intel play supporting roles, offering competitive alternatives but holding much smaller market shares. Nvidia's significance was underscored when it added nearly $200 billion to its market capitalization in a single day, simply due to strong some growth forecasts. To give you a sense of scale, the third largest public company listed on the Stockholm (Sweden) stock exchange is Investor AB with a total market cap of $94.66 billion. In other words, Nvidia had a daily market cap change more than two times the entire size of Sweden's third largest public company. Mind you, this is just the first phase of the AI value chain (revolution), and it turned a company worth $300 billion in October 2022, into a company worth $3 trillion in October 2024. This should indicate something to you with regards to the potential value appreciations forthcoming in the future phases. Nvidia is today the second most valuable company in the world by market capitalization due to selling picks and shovels for the AI gold rush. What happens when people (i.e companies) deploy these picks and shovels effectively to actually find a lot of gold as the AI value chain develops?

Alongside the chipmakers, the cloud infrastructure providers have also emerged as crucial players in this foundational phase of AI. Amazon (AWS), Microsoft (Azure), and Google (Cloud) provide immense computational power, storage capacity, and networking capabilities necessary for AI models to function and scale. These cloud giants enable the widespread deployment of AI technologies by offering flexible, scalable infrastructure that companies rely on to manage massive datasets and run intensive AI workloads. In the world of AI, they are the software backbone, supporting the rapid growth of generative AI and other advanced applications.

In short, the first phase of the AI era, Foundational Infrastructure, is shaped by two key groups; 1) NVIDIA and other semiconductor makers, providing the processing power, and 2) Cloud hyper-scalers like AWS, Azure, and Google, delivering the infrastructure to deploy and scale these technologies. Much like the gold rushes of the past, it's these providers of the "picks and shovels"—the hardware and cloud infrastructure—that are reaping the rewards in this early stage..

Why Palantir is Very Interesting When Zooming Out

Palantir is an intriguing company, because it's among very few companies that one could argue is already in the emerging application phase, due to AIP. This is the truly exciting aspect of Palantir in relation to the overall AI revolution. They have already gotten to the phase where they can model and deploy generative AI and create substantial value for their customers via their applications/platforms, thanks to the ontology layer, which took 20+ years to develop. To continue the gold rush analogy; If hardware- (Nvidia) and cloud infrastructure- providers (Amazon, Microsoft, Google) reaped rewards from the picks, shovels and transportation infrastructure, I believe Palantir is very-well placed when it comes to finding the actual gold later on (starting now already!).

As mentioned in part 1, they have created an environment and operating system for the deployment of AI models within a developed application which serve as operating systems for huge enterprises (irrespective of the type of industry), thus generating productivity and efficiency gains. This is, as far as I know, unique at this point in time. This moat will also be hard to beat for competitors, for reasons also already outlined in the first note.

LLMs as a Commodity: On Their Own, Value is Limited

As time goes by, large language models (LLMs) themselves will become more and more common, ultimately ending up as almost like a commodity. The value will be derived from being able to process and deploy these LLMs. Palantir can already do this, i.e connecting generative AI to enterprise operations. Actually, even if Palantir would stopped all R&D (which they most definitely won't) the Palantir platform would still continue to evolve. Why? Well, as LLMs constantly improve, so does Palantir's platform by definition since AIP "simply" deploys them. As an example, when ChatGPT4 becomes ChatGPT5 which then becomes ChatGPT6 (etc etc), the Foundry customers enjoy these benefits as well. Even better, they can utilize them completely within their internal environments. It's the operating system like nothing else so far.

"AI is a mysterious revolution. People basically have it wrong. They think all the value is in the large language models. Large language models are like hydrocarbons in the ground. They need to be processed" /Alex Karp

Very simply put, we can look at the AI revolution as consisting of two components; Hardware and Software.

I'm arguing that the latter might just very well have a very important player in Palantir.

Hence, the next Nvidia?

Palantir Already Ahead of the Next Curve?

Palantir is, with AIP, actually already on the next horizon of AI development, namely the use of AI agents. This is a new approach and it’s something that could change how businesses work in the future. Basically, instead of trying to build super-smart, all-knowing AI systems, Palantir is focusing on creating flexible AI systems that can delegate tasks to other tools or AI programs. This shift is significant because it allows AI to become more adaptable and useful without requiring years of development to make it super-intelligent. When you give an AI agent a task, it figures out which tools or specialized AI systems are needed to complete it. Rather than doing everything itself, the agent acts like a coordinator, selecting and managing different programs or systems. These tools can range from something simple, like a scheduling app, to more advanced AI systems designed for specific tasks.

Imagine you ask an AI agent to plan a product launch event. The agent doesn't create marketing materials or book the venue on its own, but it knows which tools to use. It could access a design tool to create promotional graphics, tap into a marketing tool to schedule social media posts, use a logistics tool to book the event space, employ another AI tool to send invitations, or even ask multiple other AI agents do some or all of the above. The AI agent isn’t directly handling each task; it's smart enough to choose the right tools and ensure everything comes together in the right order.

In short, Palantir’s AI agents represent a big shift in how AI is used, making it smarter, more adaptable, and accessible to everyone, not just tech experts.

Stock Performance, Valuation & Financials

It's very difficult to value a stock such as Palantir, as evidenced by its's very high current valuation multiples and high price volatility. A stock like Coca-Cola is easier to determine because it operates in a mature, well-established industry with predictable demand, steady earnings, and a proven business model, making it less speculative. On the other hand, Palantir is in a high-growth, innovative sector where future profitability is uncertain and heavily dependent on speculative factors like successful scaling, new technology adoption, and contract wins, which introduces a lot more uncertainty in any valuation. For this stock, I believe it's about identifying fundamentals more than anything, because if the investment thesis (found later in "Final Words") is correct, the stock will appreciate significantly in the future. How much? This is almost a guessing game for a company like this.

Just like with the introduction of ChatGPT, this radically changed the IT- and investment landscape. I certainly believe there will be more occasions similar to that one that will change the world in profound ways, we just don't know the what and when yet. If Palantir is at the forefront of some of these occasions, which I believe they are in a good position to be (and already are with Ontology and AIP), we are talking about an exciting, however uncertain, future. Be that as it may, this potential X-factor value-add is impossible to accurately estimate today.

However, based on the information available today and the current situation, I will show a current valuation with some basic DCF modelling, based on some likely and reasonable assumptions.

Is $PLTR Currently Overvalued?

The $PLTR stock has had an incredible run since the the first half of 2023 and the launch of AIP. The excitement and general AI hype has clearly played a massive role in the rise since then. As a consequence, the price multiples have skyrocketed as well, with a current price-to-earnings (P/E) ratio of 247 as of October 18th, 2024. Similarly, the price-to-sales (P/S) trades at a very high multiple as well, at around 40 times total sales revenue.

It must be stated that these are unusually high multiples. Just to give you a sense of how high they actually are at the moment, have a look at the table immediately below. Many people are puzzled by the recent surge in Palantir's stock price, often because they're looking at it through the lens of traditional valuation metrics. One key factor they might be missing is that tech stocks can remain at a very high price (or even seem overvalued) for extended periods. This is because the tech industry is often priced based on future growth potential, which can be exponential. Investors are currently banking on Palantir's anticipated growth, and the market is factoring these expectations into the stock price today. This isn't without precedent; companies like Nvidia and Amazon traded at high valuations long before their earnings justified those prices, and early investors were rewarded when those companies grew into and beyond those expectations.

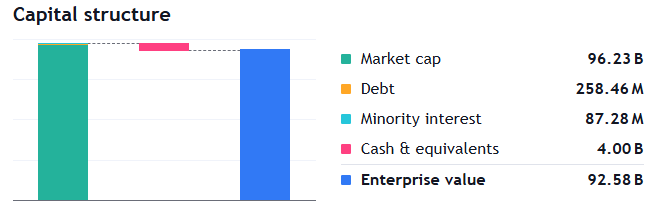

Nonetheless, the business fundamentals still look strong. Revenue is continuously increasing, margins are great, and the capital structure is excellent, with minimal debt. The risk for a share price pullback is significant in the short-term, but this might not be something entirely negative. It's normal for a stock which has had a huge price appreciation to have a "correction" where people cash out on some of the profits made. This is typical for high growth stocks.

You might have noticed that Palantir's stock doesn't move like most other stocks. Instead of gradual climbs or drops, it tends to have big spikes, sometimes jumping 50% seemingly out of nowhere. This unusual pattern can be traced back to the company's secretive nature and its involvement with government contracts. A lot of what Palantir does is under wraps due to national security concerns. This means that when they announce big news, like landing a major contract or unveiling a groundbreaking technology/application (things that I call the X-factor value-add), it can catch the market by surprise, leading to sudden jumps in the stock price.

Basic Discounted Cash Flows (DCF) and Forward Price-to-FCF Valuation

As mentioned previously, there are some innate difficulties when it comes to attempting to valuating a stock like $PLTR. The valuation comes with many assumptions, and any minor change in an important parameter (such as discount rate, terminal growth rate, revenue growth etc) can have a major impact on the estimated share price. I have made two very basic, separate discounted cash flow (DCF) valuations; Adjusted DCF and Non-Adjusted DCF. Furthermore, I have made a Forward Price-to-FCF valuation, using the two aforementioned DCF models.

The reason for having two separate DCF models is due to the fact that Palantir make adjustments in their financials with regards to stock-based compensation (SBC), associated payroll taxes for such compensation, restructuring expenses, acquisition-related expenses, and other one-off items. The stock-based compensation has been (and still is, although decreasing) a major expense, so the way this is accounted for can have a huge impact. In part 1, I discussed how the go-to-market strategy historically has involved having to employ expensive "forward-deployed" software engineers needing to be compensated partly with stocks and options, thereby diluting shareholders. Over time I believe that its very reasonable to expect the stock-based compensation to gradually decrease in relation to total revenue, but as of today it is still a significant item on the income statement.

Year and Stock-Based Compensation (SBC) | 2021 | 2022 | 2023 |

SBC as a % of Revenue | 50.5 | 29.6 | 21.4 |

With this in mind, I deemed it necessary to have two models in order to get a fair picture; one where these items are adjusted for and one where they are not. In the adjusted scenario, the forecasted number of outstanding shares also is kept the same. Vice versa, in the non-adjusted DCF the number of outstanding shares is incrementally increased year-on-year. I do this to account for dilution (or non-dilution) effects that the stock-based compensation would have in either scenario.

Discounted Cash Flow (DCF) Model: | Adjustments for stock-based compensation and one-off items/expenses? | Assumption regarding number of outstanding shares: |

Adjusted DCF | Yes | Constant. Share dilution is assumed to be reflected through adjustments for stock-based compensation instead. |

Non-Adjusted DCF | No | Incremental increase year-on-year to account for share dilution |

As you can see in the results below, both models would indicate that the stock is currently overvalued. Furthermore, the model where SBC and one-off items are adjusted for have an implied share price (34.66) that is 9.6% higher than that of the non-adjusted DCF.

The impact of SBC on the valuation, especially in the short-term, is even more clear in the forward multiple valuation based on price to free cash flow. If you pay attention to the implied share price, the difference between the two scenarios is highly significant. As an example, looking at the upper table we can see that for 2024 the difference is 29.2 - 10.3 = 18.9 USD. This is almost exclusively down to whether the SBC has been adjusted for or not. Over time, however, one can see that this differential decreases and becomes less significant.

To get the full Excel template with all my assumed assumptions and implications, click the download button below. Feel free to test different scenarios. It's all provided for FREE. All I ask of you in return is if you would be so kind to share your feedback! It would be very much appreciated on my end. If you would even sign up with your email to receive a notification whenever I release a new note, that would be even better of course! It makes a big difference in terms of supporting me.

NEW FILE FROM OCTOBER 22nd

You can see some of my key assumptions in the table below. No speculation about future products are included and this is significant because this means there is an X-factor in terms of value-add to any valuation since it's extremely plausible to assume Palantir will continue to launch some excellent products/services in the coming years. Time will tell. In 2022, this unknown X-factor would have been AIP (since it launched in 2023). I don't know what the next value-add X-factor will be, but there will surely be one or more. This is one of the most important and exciting factors to have in mind when thinking about Palantir, i.e the extremely smart and creative people working there, because this is impossible to quantify today. With this in mind, I believe my future projections are quite likely on the lower end. However, if it's by 1%, 100% or something else is today impossible to say.

Palantir is not just a tech company. It has potential to be the tech company. If it even comes close to that, "my" Excel valuations will be highly insignificant and insufficient.

Some My Key Assumptions for the DCF Models |

|---|

Total revenue growth will grow to be similar to that of the estimated total AI market growth rate of 28.46% (source: Artificial Intelligence - Global | Statista Market Forecast) |

The Commercial segment will be the key revenue driver, overtaking the Government segment. |

Operational efficiency to improve as time goes by. |

Margin improvements over time due to economies of scale and a very high customer retention rate ("sticky" product due to software integration levels). |

Network effects of the product will continuously increase, ensuring high levels of growth for the next 10-15 years. |

These are not all direct or indirect assumptions, but rather a selected few. |

Potential Network Effects of the Palantir Platform as it Evolves

The network effect occurs when a product or service gains additional value as more people use it. For the Palantir Platform, this means that as more organizations adopt its data integration and analytics tools, the platform becomes increasingly valuable. Widespread adoption leads to improved collaboration, and a richer ecosystem of third-party applications and integrations. Each new user and customer not only benefits individually but also adds value for existing users, creating a positive feedback loop that accelerates the platform's growth and utility.

This evolution mirrors how Microsoft achieved dominance. When Microsoft Windows became the standard operating system, software developers were incentivized to create applications for it, knowing they could reach a vast user base. Similarly, Microsoft Office became essential for businesses due to its widespread use and the need for compatibility in document sharing and collaboration. Applications like Microsoft Office (Excel, Word, PowerPoint etc) are clear examples of products enjoying network effects. As an example, the utility of Excel for each individual user increases as the number of users expand. This is the network effect.

As the Palantir Platform evolves, it has the potential to become the standard for data analytics and decision-making across industries. Increased adoption can attract more developers, foster a community of users who contribute to its improvement, and solidify its position as an indispensable tool. The resulting network effects not only boost the platform's total value and the utility level for each user, but also create barriers for competitors, reinforcing Palantir's market position.

Why Palantir has a Premium Valuation at the Moment

So, why does Palantir have this premium valuation right now? Palantir’s stock is on fire, and it’s not just hype. A mix of surging demand for AI, excellent products, great leadership, and a recent inclusion into the S&P 500 has positioned the company as a noteworthy player, pushing its valuation sky-high. But what’s really behind this surge? Let’s break it down.

1. AI Demand is Exploding — Just Look at Nvidia

To understand why Palantir is riding this wave, you have to look at what’s happening with AI in general. Nvidia is the poster child of this AI boom. Its GPUs power the large language models (LLMs) that are revolutionizing industries, and investors have piled in, sending Nvidia’s stock to record highs. Nvidia’s rise is the perfect proof of the market’s hunger for AI. So, if Nvidia is the "engine" of the AI revolution, Palantir is the "driver" that steers it into practical applications. And in a market hungry for AI exposure, Palantir is one of the few companies offering a direct line into this world.

2. Palantir’s Secret Sauce: AIP & Ontology

But here’s the catch: While Nvidia is building the hardware that trains AI models, Palantir is where those models actually deliver value for enterprises. Palantir’s ontology technology is the secret sauce here; it bridges the gap between cutting-edge AI and real-world business use. Without Palantir, even the most sophisticated AI models can feel like abstract concepts for enterprises.

Specifically, its Artificial Intelligence Platform (AIP) and ontology technology are the backbone of what makes AI useful for businesses. This ability to make AI functional for enterprises is something few companies can match.

With AI rapidly moving from hype to reality, Palantir has positioned itself as the go-to solution for making AI work in the real world. Investors see this as a massive opportunity because Palantir isn’t just another AI company; it’s the company that’s making AI profitable for businesses. The ability to deliver real, measurable outcomes sets Palantir apart, and this uniqueness is reflected in its premium valuation.

3. Leadership That’s Playing the Long Game

Then there’s Palantir’s leadership, which is another piece of the puzzle. Investors trust this team. They’re not just in it for quick profits, they’re focused on building something that lasts. Palantir’s founders and leaders are deeply committed to the company’s long-term vision, and that has resonated with the market. It’s rare to find a tech company where the leadership is so dedicated to creating lasting value, and that’s given investors confidence that Palantir will keep innovating and growing for years to come.

4. The S&P 500 Effect: A New Level of Demand

Another factor that’s driving Palantir’s premium valuation is its recent inclusion in the S&P 500. This is huge. It means Palantir isn’t just a hot tech stock anymore, it’s now beginning to be a staple in the portfolios of institutional investors who track the index. With this listing, big funds are required to hold Palantir stock, adding a whole new level of demand that’s pushed the stock even higher.

The S&P 500 inclusion also signals credibility. For investors who might have been on the fence, this has made Palantir an even more attractive bet.

Don't Focus on Extremely Speculative Valuation Attempts

Again, I want to make something very clear; In the grand scheme of things, the behaviour of the stock today is largely irrelevant. This is the type of stock where I almost exclusively focus on the actual investment fundamentals of the business. Based on my identified fundamentals (found in the next segment "Final Words" at the end of this note), I feel confident enough as of now to believe that the business will be worth quite a lot more in the future than what it is today. This is ultimately what matters.

Final Words

At the beginning of this long note on Palantir, starting in part 1, I asked where I where to start. Perhaps a good way to finalize this note is to borrow a quote from Alex Karp in his letter to investors in the most recent Q2 2024 financial report.

The incorporation and deployment of large language models will be one of the most telling proxy indicators of national outperformance moving forward. /Alex Karp

AI is here to stay. That’s undeniable. On a global scale, it's the next "mainstream" technology revolution. When I think about investing, my horizon isn't months or even a few years, but rather many years or decades. In that context, short-term valuations aren't as important. What matters is identifying the mega-trends and finding the companies that will lead them. That's how real portfolio value is built over time. All things considered, I believe Palantir is one of those long-term winners.

My investment thesis fundamentals for Palantir are therefore the following:

I expect Palantir to become one of the leading AI software providers; Powered by their Ontology and AIP, as well as future additional SaaS infrastructure and applications developed by the company.

The Palantir Platform will be a must-have tool for mid-to-giant enterprises across many sectors, similar to what Bloomberg is for companies and market actors in the financial sector. Not using the Palantir Platform will be too great a competitive disadvantage compared to peers.

They will successfully and continuously scale their supply side to satisfy increasing demand.

Palantir will, as time goes on, branch out to take market shares from ERP, MES, and PLM providers, as well as other adjacent sectors.

The leadership is (and will continue to be) very competent, vision-driven, and financially aligned with the shareholders.

Making this deep dive into Palantir has taken many, many days and hours, so any feedback is highly appreciated!By J

References

Accenture, 2024. The Art of AI Maturity | Accenture. [online] Available at: https://www.accenture.com/us-en/insights/artificial-intelligence/ai-maturity-and-transformation.

AWS, 2024. What are Foundation Models? - Foundation Models in Generative AI Explained. [online] Available at: https://aws.amazon.com.

Karp, A., 2024. Letter to Shareholders Q2 2024. [online] Available at: https://www.palantir.com.

Palantir, 2024. Official Website. [online] Available at: https://www.palantir.com.

Statista, 2024. Artificial Intelligence - Global | Market Forecast. [online] Available at: https://www.statista.com/statistics/941276/worldwide-artificial-intelligence-market-growth/.

The Verge, 2018. Qualcomm's LTE Modem Technology and Snapdragon Processors Powering the Mobile Revolution. [online] Available at: https://www.theverge.com.

Yahoo Finance, 2024. Palantir Technologies Inc. (PLTR) Stock Price & News. [online] Available at: https://finance.yahoo.com/quote/PLTR.

TradingView, 2024. Palantir Technologies Stock Overview. [online] Available at: https://www.tradingview.com/symbols/NYSE-PLTR/.

Morgan Stanley, 2024. Research Report on Palantir Technologies. [image].

Commentaires